It’s been a bit of a mixed bag for Liverpool supporters in

recent times. Last season the Reds finished sixth in the Premier League, while

they also reached the semi-finals of both domestic cup competitions, before

being eliminated by Aston Villa in the FA Cup and Chelsea in the Capital One

Cup.

This season looks like it might be another case of Liverpool

being the nearly men, having been narrowly beaten by Manchester City in the

Capital One Cup on penalties, while they currently lie just outside the

European places in the Premier League. They still have hopes of success in the

Europa League, having just put bitter rivals Manchester United to the sword at

Anfield, but there’s still a long way to go in that competition.

Performances have been inconsistent, the best example being

the spanking they administered to City just three days after the Wembley

defeat, which is a sure sign of a club in transition. That is indeed the case,

as Liverpool changed managers mid-season, replacing Brendan Rodgers with the

charismatic Jürgen Klopp in October.

That change came almost exactly five years after Fenway

Sports Group (FSG), the American investment company run by John W. Henry,

purchased the club in 2010. There is no doubt that the owners have brought

financial stability with the club “operating in a sustainable manner despite

the cost of football continuing to rise.”

"Boy from Brazil"

Revenue has risen every year since the FSG takeover, while the

enormous debt that the reviled former owners, Tom Hicks and George Gillett, had

placed on the club through their leveraged buy-out has been largely eliminated.

Indeed, last season FSG converted £69 million of debt into equity and invested

a further £49 million into the initial stadium expansion costs.

So the club is in far better shape financially, though

admittedly it would have been difficult to do worse than the previous

hierarchy, whose mismanagement resulted in Liverpool’s future being decided in

the High Court six years ago. That said, the club has come a long way, from the

brink of administration with the unloved Roy Hodgson as manager, to a

profitable operation with the popular Klopp at the helm.

However, FSG put their foot in it recently with the ticket

pricing fiasco. Ultimately, they backed down in the face of a major fan

backlash, so they were at least big enough to admit that they had made a

mistake, but they should never have allowed the situation to get so far that it

caused a mass walkout at one home match.

Chief executive Ian Ayre was keen to emphasise that the

owners “commitment is unwavering”, noting that they keep pumping money in and

have never taken anything out, which is a fair point, but they got it badly wrong

over the ticket prices.

"Tattooed Love Boy"

Chairman Tom Werner claimed, “We have strengthened the club

both on and off the pitch”, but in all honesty the playing record is nothing to

write home about for a club of Liverpool’s glorious history. One League Cup

(under King Kenny) and a single qualification for the Champions League is not

great, though it would have been a different story if Brendan Rodgers' side had

not fallen at the last hurdle in the 2013/14 Premier League, finishing in an

agonising second place.

Indeed, Rodgers put his finger on the challenge at

Liverpool: “The club needs to decide whether they want a business model or a

winning model. Some will think it is about buying a player, developing and

improving them and then selling them for a much greater fee; as opposed to

getting the best possible player, irrelevant of his age, in order to win.”

To be fair, Liverpool have spent significant sums on

bringing players in, but the recruits have often been of dubious quality. Some

of this has been attributed to the FSG model, featuring a transfer committee,

but it is unclear whether this “Moneyball” approach still holds sway.

Even if the club is not performing too well on the pitch, it

is tearing it up off the pitch, as evidenced by the recently published 2014/15

accounts, which featured a massive £60 million profit before tax, up £59

million from the previous year’s £1 million profit.

Ian Ayre said that this was “mainly a result of the sale of

Luis Suarez in July 2014”, which increased the profit on player sales by £57

million, though the revenue growth was also impressive, up £42 million (17%)

from £256 million to a record £298 million.

Broadcasting revenue was £22 million (22%) higher at £123

million, mainly due to Champions League participation and the domestic cup

runs. The additional home games also helped drive an £8 million (16%) increase

in match day revenue to £59 million.

Commercial income rose £13 million (12%) to £116 million,

due to additional sponsorship from 12 new partnerships and renewals and higher

merchandising sales following the opening of 180 new retail outlets around the

world including one standalone store in Malaysia.

These improvements were offset by significant increases in

player costs: the wage bill surged £22 million (16%) from £144 million to £166

million, while player amortisation was up £20 million (48%) from £41 million to

£61 million.

On the other hand, a small credit for stadium development

costs meant that exceptional items were £2 million lower, while net interest

payable fell £1 million to £4 million.

As Ayre observed, “the club is in rude health financially”,

which is confirmed by Liverpool’s £60 million being by far the highest profit

of the 14 clubs that have to date published their 2014/15 accounts. The next most

profitable clubs are Leicester City £26 million, Arsenal £25 million and

Southampton £15 million.

Although football clubs have traditionally lost money, the

increasing TV deals allied with Financial Fair Play (FFP) mean that the Premier

League these days is a largely profitable environment with only four clubs

losing money so far in 2014/15, the largest losses coming from Aston Villa £28

million and Chelsea £23 million.

That said, it is far from unusual for Premier League clubs

to report lower profits in the second year of the television deal’s three-year

cycle, as there are limited possibilities for revenue growth, while wage bills

continue to grow apace. In fact, half of the clubs that have announced 2014/15

figures have reported lower profits, which makes Liverpool’s £59 million growth

all the more impressive.

However, it is clear that once-off profits from player sales

can have a major influence on a football club’s bottom line, especially at Liverpool,

whose numbers were boosted by £56 million from this activity in 2014/15,

compared to a £1 million loss the previous year.

The lion’s share of this profit was obviously from Suarez’s

sale to Barcelona, but the club also earned money from the transfers of Oussama

Assaidi to Al-Ahli Dubai, Daniel Agger to Brøndby and Martin Kelly to Crystal

Palace.

This is the second year in succession that Liverpool have

reported a profit, following five years of losses that amounted to a hefty £176

million, including an average of £47 million for the three seasons between 2011

and 2013.

In fairness, many of these losses were caused by FSG having

to spend substantial sums on player recruitment in order to repair the damage

caused by the previous owners’ lack of investment in the squad. It should also

be noted that the 2011/12 accounts only included 10 months after the club moved

the accounting date to 31 May.

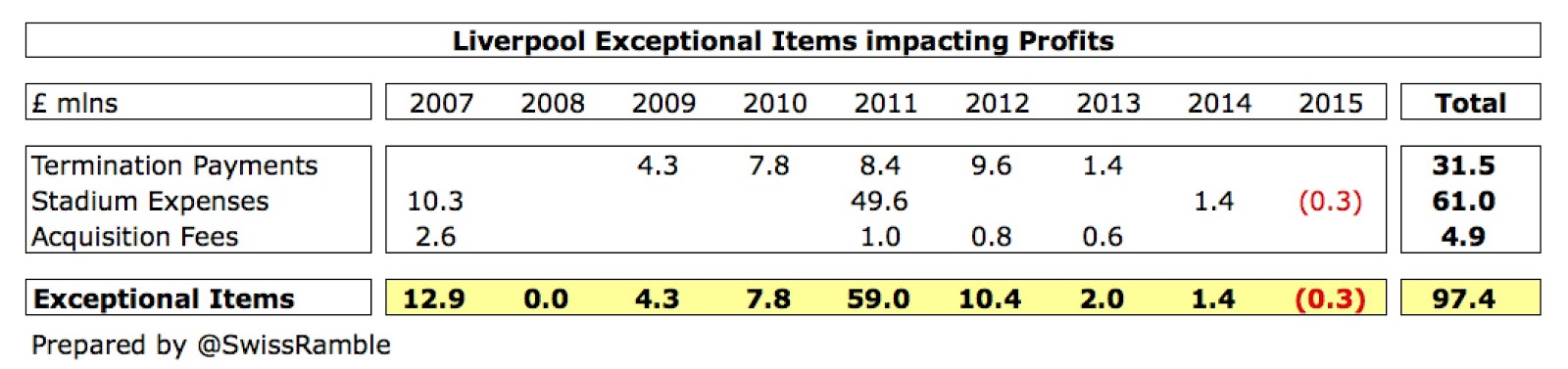

The other factor that has had a strong influence on

Liverpool’s losses is the amount booked for so-called exceptional items, which

adds up to nearly £100 million over the last nine years, mainly due to

writing-off £61 million spent on unsuccessful stadium developments and £31

million paid-out as a result of changes in coaching staff (e.g. the departures

of Roy Hodgson and Kenny Dalglish). There were also £5 million of legal and

professional fees incurred as a result of FSG’s purchase of the club.

In fact, Liverpool would have made a profit of £10 million

in 2011 without such exceptionals. These have been steadily reducing and actually

produced a £0.3 million credit in 2014/15 against costs previously booked for

the stadium development in Stanley Park, though next year’s accounts should

include a sizeable payout to former manager Brendan Rodgers, who had three

years remaining on his deal when he was sacked.

Profits and losses have also been greatly influenced by

player trading. In the six seasons up to 2011, player sales boosted profits (or

at least reduced losses) by an average of £18 million a year. This was most

evident in 2011 when £43 million of profits on player sales, mainly Fernando

Torres to Chelsea, reduced the annual loss from a horrific £93 million to

“only” £49 million, though, as we have seen, that was also affected by £59

million of exceptional stadium costs.

However, the club’s ineptitude in the transfer market

resulted in three consecutive years of losses on player sales between 2012 and

2014, most notably the sale of Andy Carroll to West Ham.

That drag on the club’s financials spectacularly changed in

2015 with the Suarez sale and we already know from a note in the accounts that

the 2016 figures will include £41 million of profits from player sales, mainly the

lucrative sale of Raheem Sterling to Manchester City plus Fabio Borini’s

permanent move to Sunderland.

"Can you feel the beat?"

Ayre is perfectly aware of the influence of player sales:

“Our real financial position is closer to break-even and it is the underlying

revenue growth that’s important and provides us with the long-term stability.”

Indeed, excluding the £56.2 million made from player sales in 2015 would leave only

a small £3.8 million profit.

It is worth exploring how football clubs account for

transfers, as this can have such a major impact on reported profits. The

fundamental point is that when a club purchases a player the costs are spread

over a few years, but any profit made from selling players is immediately

booked to the accounts.

So, when a club buys a player, it does not show the full transfer

fee in the accounts in that year, but writes-down the cost (evenly) over the

length of the player’s contract. To illustrate how this works, if Liverpool

paid £25 million for a new player with a five-year contract, the annual expense

would only be £5 million (£25 million divided by 5 years) in player

amortisation (on top of wages).

However, when that player is sold, the club reports the

profit as sales proceeds less any remaining value in the accounts. In our

example, if the player were to be sold three years later for £32 million, the

cash profit would be £7 million (£32 million less £25 million), but the

accounting profit would be much higher at £22 million, as the club would have

already booked £15 million of amortisation (3 years at £5 million).

This is all horribly technical, but it does help explain how

it is possible for clubs like Manchester City to spend so much and still meet

UEFA’s FFP targets.

Notwithstanding the accounting treatment, basically the more

that a club spends on buying players, the higher its player amortisation. Thus,

Liverpool’s player amortisation has shot up from £34 million in 2012 to £61

million in 2015, reflecting renewed activity in the transfer market. It should

be even higher next year, as this figure does not reflect last summer’s

purchases of Christian Benteke, Roberto Firmino and Nathaniel Clyne.

Liverpool have also booked around £20 million of impairment

charges in the last four seasons, though the vast majority was in 2012 and 2013.

This happens when the directors assess a player’s achievable sales price as

less than the value in the accounts.

Despite rising by nearly 50% in 2015, Liverpool’s player

amortisation of £61 million is still surpassed by the really big spenders like

Manchester United, whose massive outlay under Moyes and van Gaal has driven

their annual expense up to £100 million, Manchester City £70 million and

Chelsea £69 million, but it is now ahead of Arsenal £54 million.

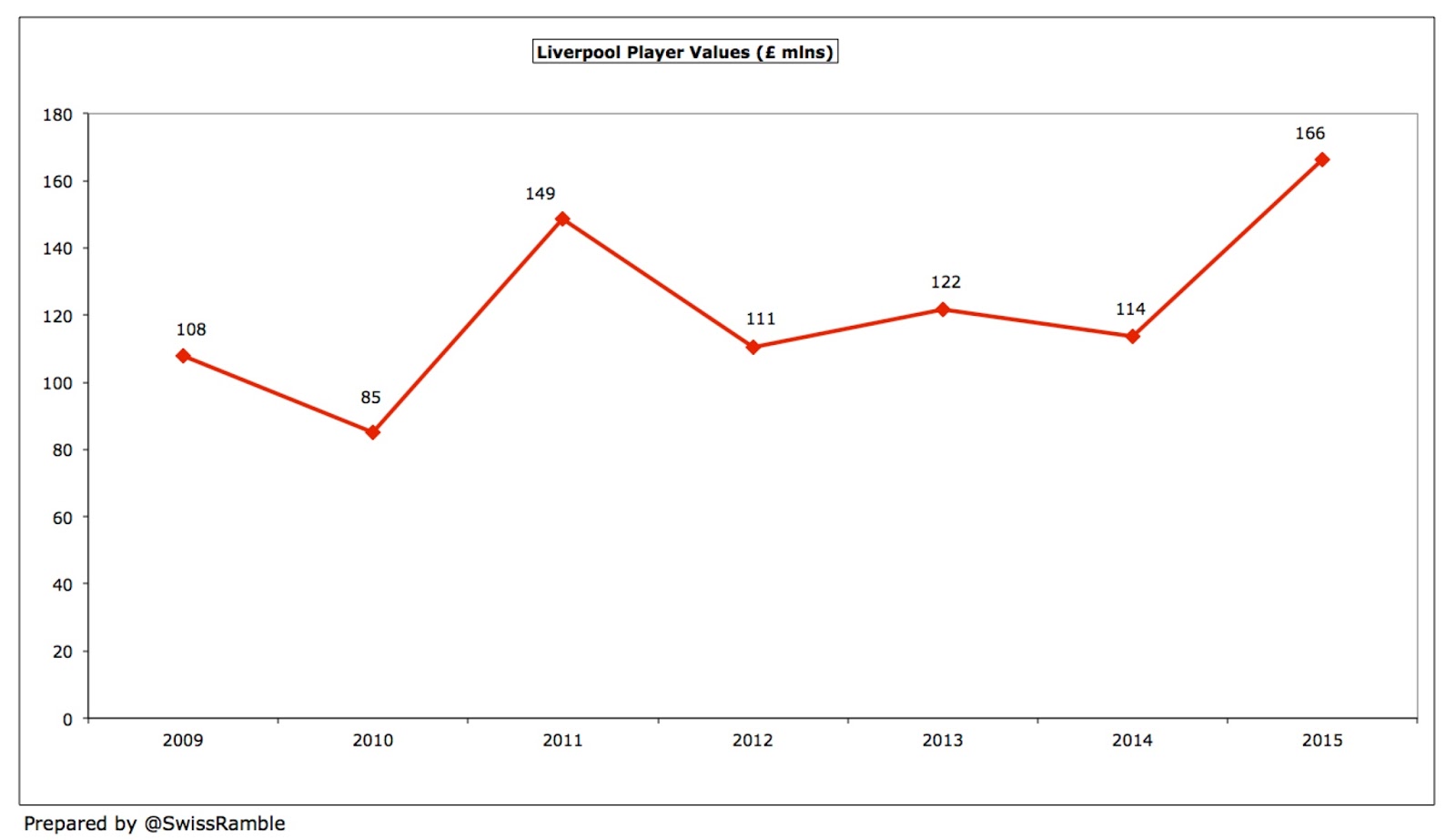

The other side of the player trading coin is that player

values have also shot up, nearly doubling from £85 million in 2010 to £166

million in 2015.

As a result of all these accounting shenanigans, clubs often

look at EBITDA (Earnings Before Interest, Depreciation and Amortisation) for a

better idea of underlying profitability. In Liverpool’s case this metric

highlights the major improvement in their finances, as it is has steadily risen

from £10 million in 2011 to a very healthy £73 million in 2015.

That’s excellent and is only outpaced by the two Manchester

clubs, United £120 million and £83 million, but Liverpool are actually ahead of

Arsenal, the poster child of profitability in English football, at £63 million.

However, before people get too complacent, United are

projecting astonishing EBITDA of £178-188 million for 2015/16, following their

return to the Champions League and their new kit deal.

Revenue has grown by 61% (£113 million) since FSG took over

in 2010, though most of this (£92 million) has come in the last two seasons

with revenue being relatively flat over the previous seasons. As Ayre stated,

“growth in our commercial, media and match day revenues…continues to add

strength to out financial position.”

The main growth driver has been commercial income, which has

increased by 87% (£54 million) over that period, though broadcasting is also up

54% (£43 million), largely due to the new Premier League TV deals. Match day

income has, perhaps surprisingly, also risen by 38% (£16 million).

Even after the 2015 revenue growth, Liverpool remain in

fifth place in the English revenue league with £298 million, though they have

closed the gap to the top four. Nevertheless, they are still almost £100

million behind Manchester United (£395 million) and over £50 million lower than

Manchester City (£352 million).

They are also below Arsenal (£329 million) and Chelsea (£314

million), but are a long way ahead of their other Premier League rivals, being

£100 million higher than Tottenham (£196 million) and around £170 million

higher Newcastle United (£129 million).

This is the reason for many Liverpool fans’ frustration, as

they should have enough spending capacity to do better than the likes of Spurs

(and Leicester City), even if they might expect to struggle from a financial

perspective against the top four.

In fact, Liverpool’s revenue growth of £42 million (17%) was

easily the best of the leading six English clubs last season, both in absolute

and percentage terms. United actually saw a £38 million (9%) decline, due to

their failure to qualify for Europe, while Chelsea’s revenue also dropped £6

million (2%).

Of course, the boot will be on the other foot next year, as

United made their return to the Champions league, while Liverpool only

qualified for the Europa League.

Liverpool comfortably retained ninth place in the Deloitte

Money League, though the gap to Juventus in 10th place increased from £22

million to £52 million, partly due to the strengthening of Sterling against the

Euro. However, even excluding currency movements, Liverpool enjoyed the second

highest revenue growth in the Money League last season, only beaten by

Barcelona.

That’s obviously a fine accomplishment, but the Money League

highlights a new challenge for clubs like Liverpool, as no fewer than 17

Premier League clubs feature in the top 30 clubs worldwide by revenue, thanks

to the TV deal. This means that the mid-tier clubs have more purchasing power

than ever before, so are more competitive as a consequence.

If we compare Liverpool’s revenue with the other clubs in

the Deloitte Money League top ten, it is immediately apparent where their main

problem lies, namely commercial income. Liverpool’s £116 million might seem

pretty good, but it is substantially lower than most of the elite clubs.

Granted, the £110 million shortfall against PSG (£116

million vs. £226 million) is largely due to the French club’s “friendly”

agreement with the Qatar Tourist Authority, but there are still major gaps to

the other clubs in commercial terms: Bayern Munich £95 million, Manchester

United £84 million, Real Madrid £72 million, Barcelona £69 million and

Manchester City £57 million.

This makes it all the more perplexing that the owners would

focus on match day income and try to “nickel and dime” the community, when the

larger opportunity is surely in the commercial arena.

On the plus side, Liverpool are very competitive on

broadcasting revenue, only really losing out compared to the individual deals

negotiated by Real Madrid and Barcelona, and Juventus, who were boosted by

particularly high Champions League distributions last season.

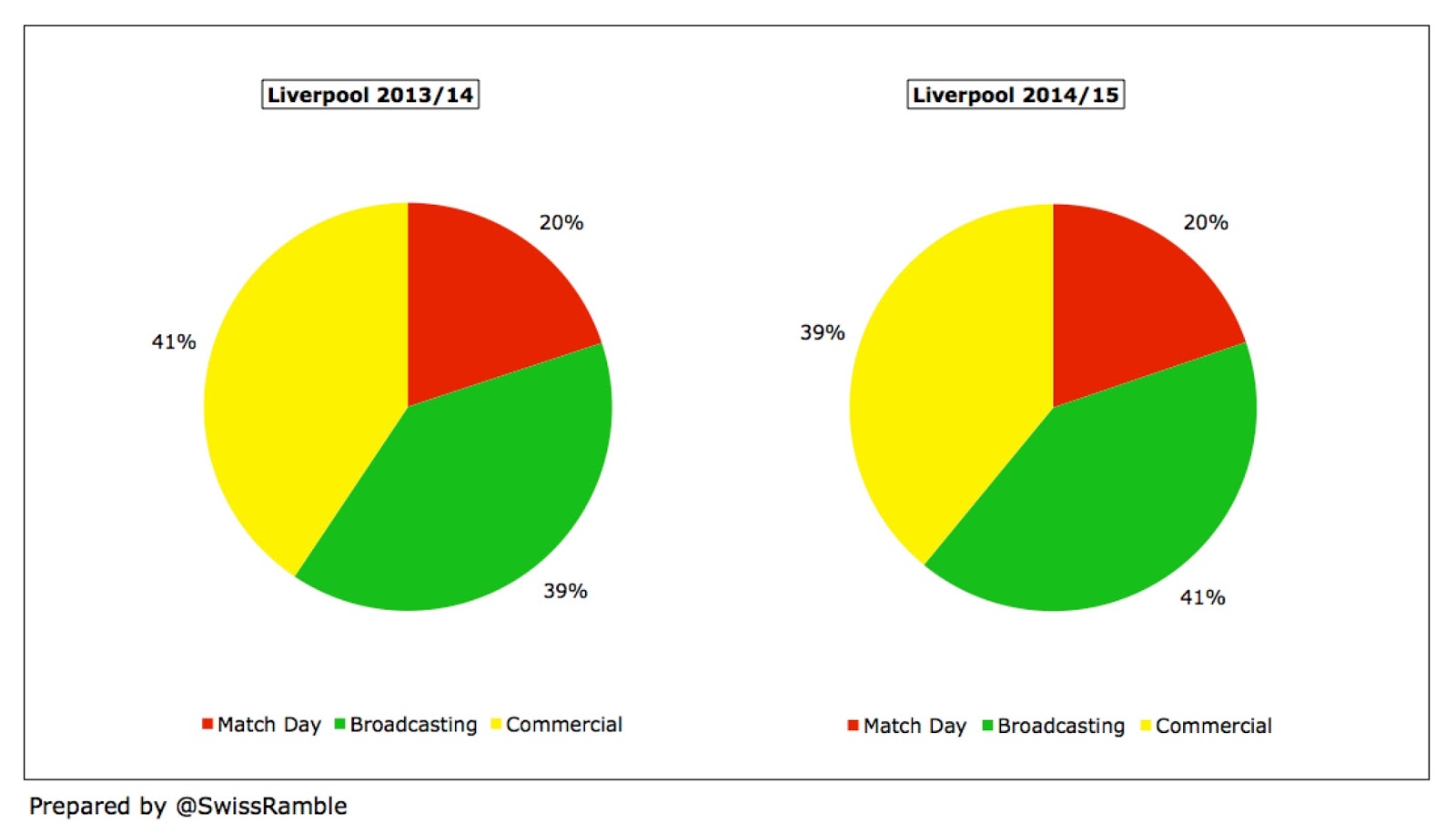

Actually, match day only accounts for 20% of Liverpool’s

total revenue with broadcasting (41%) and commercial (39%) far more important,

following the huge growth in these revenue streams.

Liverpool’s share of the Premier League television money fell

£5 million from £98 million to £93 million in 2014/15, largely due to lower

merit payments for only finishing in 6th place in the league, as opposed to

finishing second the previous season.

The only other variable element in the Premier League

distribution is the facility fee (also 25% of the domestic deal), which depends

on how many times your team is broadcast live. Liverpool always do well here,

due to their box office appeal. All other elements are equally distributed

among the 20 Premier League clubs: the remaining 50% of the domestic deal, 100%

of the overseas deals and central commercial revenue.

Of course, there will be a substantial increase from the

mega Premier League TV deal starting in 2016/17. My estimates suggest that

Liverpool’s 6th place would be worth an additional £46 million under the new

contract, taking their annual payment up to an incredible £138 million. This is

based on the contracted 70% increase in the domestic deal and an assumed 30%

increase in the overseas deals (though this might be a bit conservative, given

some of the deals announced to date).

The other main element of broadcasting revenue is European

competition with Liverpool receiving €33.6 million for Champions League

participation plus an additional €0.5 million after dropping down to the Europa

League, where they were eliminated by Besiktas.

Here it is worth noting the importance of the TV (Market)

pool to the Champions League distributions. Half of the payment depends on how

far a club progresses in the Champions League, but also how well the other

English clubs do. In this way, Liverpool’s share was smaller than the other

English clubs, as they went out at the group stage, while the others reached

the last 16.

The other half of the market pool is based on where the club

finished in the previous season’s Premier League, so Liverpool did well here,

as they finished 2nd in 2013/14, giving them a 30% share (1st 40%, 3rd 20%, 4th

10%).

Incidentally, the reason why Juventus received such an

enormous slice of the Italian market pool is that they only had to share it

with one other club (AS Roma), while the UK pool was split between four clubs.

Having won the European Cup/Champions League five times,

nobody needs to explain its importance to Liverpool, but the club’s failure to

qualify for Europe’s premier tournament more than once in the last five years

has really hurt their bank balance.

In that period, Liverpool have earned €45 million from

Europe, which is around €100 to €180 million less than the top four received –

and that does not include revenue from additional fixtures and sponsorship

clauses. That’s a huge competitive disadvantage and makes it all the more

difficult for Liverpool to break into the Champions League qualifying places.

The financial significance of a top four placing is even

more pronounced from this season with the new Champions League TV deal worth an

additional 40-50% for participation bonuses and prize money and further

significant growth in the market pool thanks to BT Sports paying more than

Sky/ITV for live games.

Match day income grew by £8 million (14%) from £51 million

to £59 million, mainly due to seven more home games from European competition

and domestic cup runs, with the average attendance virtually unchanged at

44,659. This means that match day income has increased by a total of £14

million in the last two seasons.

That’s good news, but Liverpool’s match day income is still

miles behind Arsenal (£100 million) and Manchester United (£91 million). In

order to address this difference, FSG plan to expand the Main Stand capacity by

8,500 seats taking the overall Anfield capacity to around 54,000, which should

be complete for the 2016/17 season. Potentially, there would also be a further

increase of 4,800 seats in the Anfield Road stand at a later date.

It is estimated that this would increase revenue by £25

million: £20 million from the extra seats and £5 million for naming rights for

the stand, though a partner is still not in place. Importantly, the club would

keep the famous Anfield name for the stadium as a whole.

This project will cost well over £100 million, but it is

likely to be funded by an interest-free loan from the owners, thus eliminating

the need to make steep interest payments. Indeed FSG has already loaned the

club £49 million for the initial expenditure.

Ayre stressed the importance of the stadium expansion: “The

new Main Stand at Anfield is another significant investment by this ownership

which is vital to the health of the club and part of our long-term strategy to

ensure we remain competitive and sustainable.”

He added, “It gets us towards the capacity we want, and at a

better cost than building a new stadium”, though the 25,000 fans on Liverpool’s

season ticket waiting list may have preferred the more expansive option.

"Miss You"

Although this all sounds very promising, especially given

the numerous false starts in the past, it does not really excuse the owners not

addressing the supporters’ concerns over ticket prices, especially in light of

the growing TV riches. This is a great opportunity for football clubs to make prices

more affordable and avoid the traditional fan base being priced out.

According to the BBC Price of Football survey, Liverpool

have the fourth most expensive cheapest season tickets, only behind the big

London clubs (Arsenal, Tottenham and Chelsea), but there is obviously a vast

salary gap between those two markets.

While it is understandable that the board would want to

narrow the match day income gap, the stadium expansion will go a long way

towards that without price gouging the fans. In any case, the owners finally

recognised the value of the supporter base and abandoned their plans and froze

prices. That said, that gesture has since been effectively trumped by Everton

actually reducing ticket prices by 5%.

Commercial revenue rose £12 million (12%) from £104 million

to £116 million, mainly due to additional sponsorship and merchandising sales.

New sponsor deals included Garuda (training kit), Subway and Dunkin’ Donuts, which

is an example of Liverpool’s stated strategy of “leveraging the club’s global

following to deliver revenue growth.”

Liverpool’s commercial income has overtaken Chelsea (£108

million), though the Blues will be boosted next season by their new shirt deal

with Yokohama Tyres, but it is still a long way below Manchester United £197

million and Manchester City £173 million.

To reinforce this point, Liverpool’s commercial income

growth of £36 million over the last three seasons is only better than Tottenham

of the leading English clubs. In the same period, Manchester United have

increased their commercial income by £79 million – and that’s before United

receive the full benefit of their massive new Adidas kit deal. In fact, the gap

between Liverpool and United has grown from £10 million in 2009 to £81 million

in 2015.

Liverpool have extended their shirt sponsorship deal with

Standard Chartered by three years to the end of the 2018/19 season, increasing

the annual payment from £20 million to £25 million (though some reports suggest

that this might be as high as £30 million). That’s not too bad, but is lower

than Manchester United £47 million (Chevrolet), Chelsea (Yokohama) £40 million

and Arsenal (Emirates) £30 million.

Liverpool’s “record” New Balance kit deal is basically worth

the same amount as the six-year deal signed with Warrior in 2012, namely £25

million a season, with the increase coming from the other part of the deal,

i.e. earnings from merchandising sales, due to New Balance’s better

distribution network.

Whatever the exact details, it is still lower than

Manchester United’s “largest kit manufacture sponsorship deal in sport” with

Adidas, which is worth £750 million over 10 years or an average of £75 million

a year from the 2015/16 season.

Wages increased by £22 million (16%) from £144 million to

£166 million, though the underlying growth is even higher, as the previous

season included high bonus payments “as a result of the impact of the 2nd place

Premier League finish.” The number of employees rose from 567 to 636, largely

in the administration, commercial and other department.

The highest paid director, presumably Ayre, received an

inflation-busting 16% pay rise from £1.0 million to £1.2 million, which is nice

work if you can get it.

Despite this wages growth, the wages to turnover ratio was maintained

at a very respectable 56%, which is around the same level as the likes of

Arsenal (58%), Tottenham (56%) and Manchester City (55%).

Liverpool’s £166 million is the 5th highest wage bill in

England, exactly in line with revenue. Chelsea once again have the highest wage

bill in the top flight at £216 million, which is the first time since 2010,

ahead of Manchester United £203 million, Manchester City £194 million and

Arsenal £192 million. There is then a big gap to the other Premier League clubs

with the nearest challengers being Tottenham (2013/14) £100 million and Aston

Villa £84 million.

What is interesting is how the wage bills at the top four

clubs have been converging around the £200 million level. Both Manchester clubs

actually saw a reduction in wages in 2014/15. United’s decrease was due to

their lack of success on the pitch, as bonuses fell, while City’s is partly due

to a group restructure, where some staff are now paid by group companies, which

then charge the club for services provided.

Liverpool’s gap to Arsenal in 4th place has remained fairly

constant over the last there seasons at around £25 million.

The different investment policies of the last two sets of

owners can be clearly seen by looking at the net transfer spend: in the five

years leading up to the FSG takeover the club averaged net spend of just £10

million, but this has tripled to £30 million in the five years since then, even

after a number of big money sales including Torres and Suarez.

It was imperative that Fenway splashed the cash after Hicks

and Gillett kept their hands in their pockets and they have done so. In the

2014/15 season alone, Liverpool bought Adam Lallana, Lazar Markovic, Dejan

Lovren, Mario Balotelli, Alberto Moreno, Emre Can, Divock Origi and Rickie

Lambert.

As Ayre said, “We are very fortunate in that everything we

generate goes back into the team”, though many would argue that the proceeds of

the Suarez sale have not been wisely reinvested, as there seems to have been a

focus on quantity rather than quality. Furthermore, Liverpool spent more last

year on agents’ fees (£14.3 million) than any other club in the top flight,

which is a fairly damning indictment.

Even with the increased activity in the transfer market,

Liverpool have still been significantly outspent by some clubs over the last

three seasons, maybe understandably by Manchester City £241 million, Manchester

United £199 million and Arsenal £111 million, but also by West Ham £79 million.

They have also been nearly matched by Newcastle £71 million, Everton £65

million and Crystal Palace £65 million.

Legendary Liverpool defender Alan Hansen suggested that the

club would need to spend £200 million “to have a real go”, but he cautioned, “From

what I understand FSG have told the manager it is not a bottomless pit. So the

problem Klopp might have is that the owners have invested so much already, will

they be reluctant to do it again?”

Gross debt has reduced by £28 million from £127 million to

£99 million, comprising bank loans of £50 million (down from £58 million) and

£49 million from the owners in order to fund stadium expansion work. Note that

the reported net debt excludes £20 million owed to the subsidiary

Liverpoolfc.TV Limited.

The previous £69 million owed to FSG has been converted into

equity. As Ayre said, “It’s effectively writing-off that debt for the club and

putting us in a healthier position. It’s another great example of the

commitment that the owners make to the club.” The owners would only get this

money back if they were to sell the club.

Maintaining their customary position, Liverpool’s gross debt of £99 million is the 5th highest in the Premier League, though is much less than Manchester

United, who still have £444 million of borrowings even after all the Glazers’

various re-financings, and Arsenal, whose £232 million debt effectively

comprises the “mortgage” on the Emirates stadium.

It is also worth highlighting that the club’s debt position

is stratospherically better than the shocking levels reported under the

previous owners. While there was “only” £123 million net debt in the football

club, the full picture was revealed in the holding company where borrowings had

grown to nearly £400 million. Fortunately, this debt was largely eliminated

following the change in ownership.

In addition to this debt, Liverpool have contingent

liabilities of £13 million, which represent fees that may be payable depending

on contractual clauses such as number of appearances, Champions League

qualification, etc. Similarly, Liverpool will potentially receive £4 million

from other clubs. The accounts also note that the net amount payable in

transfer fees arising from this summer’s transfer is £37 million.

It is worth noting that the net interest payable of £3.6

million has come down significantly since the bad old days of Hicks and Gillett,

when it peaked at £17.6 million in 2010. As a comparison of what might have

been, Manchester United incurred £35 million of interest costs last season as

the price of their leveraged buy-out, while Arsenal have net financing costs of

£13 million.

The amount of cash Liverpool generate from operating

activities has been increasing, reaching £65 million in 2015, after adding back

non-cash expenses like player amortisation and depreciation. Nevertheless, they

still required £49 million of funding from FSG to cover their cash outlay, as

they spent a net £59 million on players (gross £96 million), £40 million on the

stadium development, £9 million on bank loan repayments and £3 million interest

payments.

In the five years since FSG bought Liverpool, the club has had

available cash of £320 million. Less than half of this (£146 million) has come

from operating activities, while £114 million has been provided by the owners

in the form of loans and a further £46 million from the bank facility.

Nearly two-thirds of this funding has been seen on the pitch

with £211 million spent on net player recruitment, while another £55 million

went on infrastructure investment. An outstanding stadium loan of £38 million was

repaid, while £16 million of interest payments on external bank loans have been

required.

Unlike other American owners, FSG cannot be accused of

hoarding cash, as Liverpool only have £4 million in their bank account. In

stark contrast, Arsenal had £228 million and Manchester United £156 million.

It is difficult to disagree with Ayre’s view that Liverpool are

“making good progress”, but the question remains whether the club can break into

the top four, given that it is ranked fifth in just about very category

(revenue, attendance, wage bill, debt).

Whether Klopp is given enough funding to successfully

overhaul his squad is debatable, but at least Liverpool now have a manager that

everybody can get behind. Not to mention the fact that the German has already demonstrated

his ability to revive a sleeping giant at Borussia Dortmund.

"I'm in love with a German film star"

The owners are keen to stress that they are ambitious to win

trophies: “We have great conviction in our world-class manager and our young,

talented squad and know that in time the on-pitch success we all crave will be

realised.”

That’s easier said than done, of course, but after a period of stability, Klopp might just be the man to bring the glory nights back to Anfield. Whichever way it goes, it’s sure to be an exciting ride.

That’s easier said than done, of course, but after a period of stability, Klopp might just be the man to bring the glory nights back to Anfield. Whichever way it goes, it’s sure to be an exciting ride.

As ever a fascinating trawl through the numbers, obviously the nature of the annual account time frame means we are all looking at what is now part of the historical context of a rather brighter present. The stadium expansion is rapidly taking shape, the 2015 transfer spend looks (Benteke aside) much more sensible than that of 2014 (though its worth noting that Lovren, Can, Origi and Lallana are all contributing more under Klopp) while Sterling's sale looks like smarter business every day. Hopefully the expanding Chinese game can at least minimise losses on Balotelli and Benteke is certainly a good player for a different team.

ReplyDeleteThe lack of CL football is painful no question such are the riches for just reaching the group stages when compared to the poverty stricken Europa League (surely it's in UEFAs own interests to try and boost that financially and not just in terms of prestige, vis-a-vis CL qualification)

As I type Klopps side are once again tantalisingly close to 4th place in the league (thanks to that game in hand) but unless the team goes on a run to the end of the season it's surely out of reach.

Hi. Great blog. What is your take on a possbile Superleague? What changes would you make to the Champions League model?

ReplyDeleteIt seems like the growth of the Premier League will force the rest of European football to react, somehow (even Bayern is getting nervous).

You had me at "Liverpool - Over the wall"

ReplyDeleteno rea; surprise. the US can make money, but cant manage a succesfull FOOTBALL club, the "money ball" example made Lfc 9th richest in Europe, doesnt fill me with joy, when the football team fell from TOP to 46th in the UEFA rankings. Klopp obviously hired due to henrys expectation that he will make squad palyers into champions ; Maybe Atletico and Leicester give hope on that score. True REds would rather be more in debt , and top of the league! we shall see!

ReplyDeleteThat fall was largely the result of Gillett and Hicks shoddy ownership plus Rafa Benitez leaving (itself a fall out of G & H), when a club tumbles now it tumbles hard. Meanwhile FSG are backrolling a stadium expansion and spent 32.5 on a managers whim (Benteke). The good news is that Klopp is about 10 times the manager that Rodgers is

DeleteAnfield Wrap linked us here. Amazing detail and really well written.

ReplyDeleteGot to know the exact graph of performance of Liverpool... so nice blog!!!

ReplyDeleteHow do you work out:

ReplyDelete- Player Depreciation (Through the years) ?

- Increase in Players Value (Through the years) ?

Thanks

One can't work out a genuine increase in value until a bid is made. Though the market can suggest an estimate by way of players of similar profile being sold.

DeleteDepreciation is worked out as dividing the transfer fee by the contract length (obviously one might have to take account of clauses that are triggered during the contract - winning a title for example) so 25m player on 5 year deal means his value is calculated as 25/5 - 5 million per year.

FSG looking to pack their bags and sell up possibly? I can see it. Not too many football clubs have figures as good as these. Maybe preparing to sell before figures get worse?

ReplyDeleteWhy will the figures get worse. New TV deal, £25 mill more from the new stand,lots of commercial contracts are coming up for renewal. Outline plans for further expansion of Anfield in the pipeline. A new manager who will only increase the appeal of the club in existing and new markets. Still plenty to tap and to add value before they cash in, if that is their long term ambition.

ReplyDeleteCool

ReplyDelete