Many Arsenal fans have been unhappy for the past few years

about the lack of trophies, exacerbated by the club’s seeming inability to

spend its growing cash balance. Therefore, they should have been pleased by the

results both on and off the pitch last season, as Arsenal won the FA Cup (for

the 11th time) after defeating Hull City 3-2 in a thrilling final,

qualified for the Champions league for an extraordinary 17th

successive season and also obliterated their transfer record when buying the

German star Mesut Özil from Real Madrid.

As Chief Executive Ivan Gazidis said when announcing the

financial results for the 2013/14 season, “Our improved financial position has

allowed us to supplement the squad with important new signings.” Indeed,

Arsenal continued to spend big this summer, bringing three World Cup stars to

the Emirates in the shape of Alexis Sanchez from Chile, Mathieu Debuchy from

France and David Ospina from Colombia. In addition, the club’s English core was

again strengthened by acquiring Danny Welbeck from Manchester United and the

highly promising Calum Chambers from the much-vaunted Southampton academy.

However, there remains a nagging feeling that Arsenal are

still not maximising their potential or making use of their bountiful financial

resources, as the squad still looks worryingly thin in defence, while the need

for a powerful presence in midfield seems obvious to all but the most stubborn.

The supporters’ concerns were hardly eased by last week’s feeble capitulation

to a rampant Borussia Dortmund side in the aforementioned Champions League.

Arsenal’s accounts once again emphasised the club’s

financial strength, as revenue exceeded £300 million while the club reported a

profit for the 12th year in a row, another amazing achievement.

Although the profit before tax of £4.7 million was virtually unchanged from the

previous year’s £6.7 million, the way that the club reached this profit figure

was very different.

Revenue from football activity surged £56 million (23%),

largely thanks to the new Premier League TV deal, which was worth an additional

£36 million, plus increasing commercial income (up £15 million), mainly due to

including a full year of the extended Emirates sponsorship deal, and £7 million

higher match day income, driven by three more home games.

This offset a £12 million increase in the wage bill (up to

£166 million) and a significant £40 million reduction in profit from player

sales from £47 million to £7 million. The only meaningful money generated this

season came from the sales of Gervinho to Roma and Vito Mannone to Sunderland,

while last year’s accounts included the far more lucrative departures of Robin

van Persie to Manchester United and Alex Song to Barcelona.

"Don't Let Me Be Misunderstood"

Player amortisation (the annual cost of expensing transfer

fees) was around the same level at £40 million, but profits were boosted by no

player impairment (reducing the carrying value of players in the accounts) this

season compared to £6 million in 2012/13.

Other operating expenses rose £8 million to £70 million,

partly due to an increase in revenue-related costs, such as staging more games

at the Emirates and supporting commercial partnerships.

Profit after tax for 2013/14 was £7.3 million, mainly thanks

to a net £2.6 million tax credit linked to the reduction in the corporation tax

rate to 20% from April 2015, thus reducing the club’s deferred tax liabilities.

That’s fairly technical, but it’s basically good news.

Of course, it’s not unusual for Arsenal to report a profit. In

fact, the last time that the club made a loss was way back in 2002, a virtually

unparalleled feat in the world of football where most success is effectively

bought. Every now and then we see an exception, such as Atletico Madrid’s

glorious efforts last season, but the normal rule is that money talks. In

Arsenal’s case, they have made combined profits of over £200 million in the

last seven years.

The Premier League accounts for the 2012/13 season amply

demonstrate how rare this is, as only eight clubs made money, while many others

reported massive losses. Of particular interest to Arsenal would have been the

figures registered by those clubs that finished above Arsenal in the league

table with Manchester City, Chelsea and Liverpool all losing around £50 million.

That said, Manchester United’s 2013/14 results highlight

that Arsenal still have a long way to go to compete on a level playing field

with the financial elite. As Arsenal’s football revenue approaches the £300

million level, United are already generating a hefty £433 million, i.e. an

additional £133 million every

season, and that’s before United’s spectacular £750 million adidas deal, which

only commences in August 2015.

So what, you might say, but here’s the thing: this ability

to throw off cash allowed United to spend £215 million on wages, which is £48

million more than Arsenal – and they still reported a much higher profit before

tax of £24 million (£17 million higher than Arsenal). The majority of

right-thinking football fans would not endorse the Glazers’ approach to owning

a football club, but without the interest payments arising from their leveraged

buyout (£27 million last season) United’s spending capacity would be even

higher. You can’t rely on the Moyes effect every year.

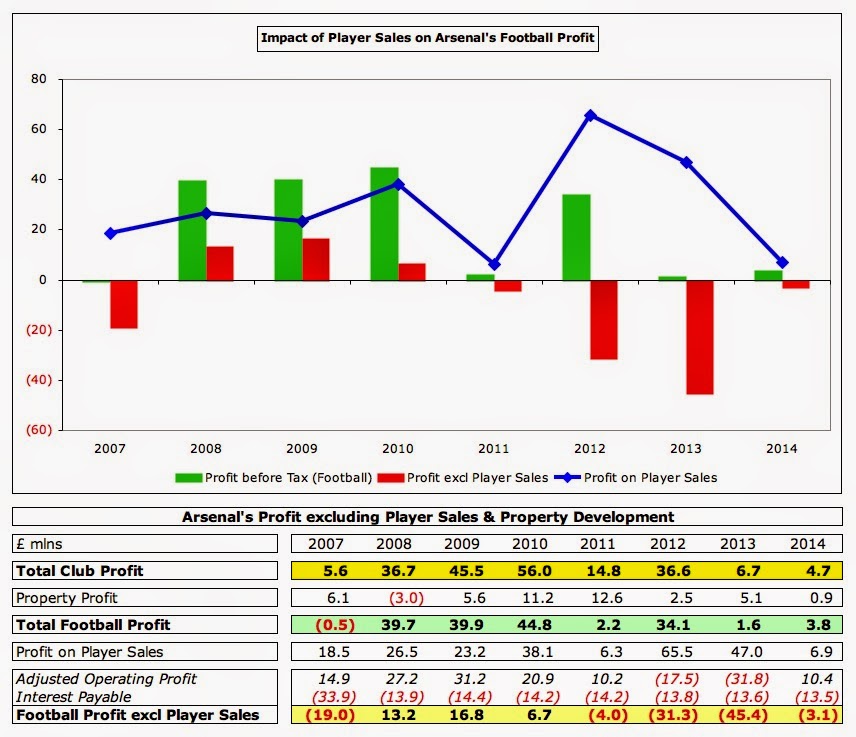

What is encouraging for Arsenal is that they are no longer

so reliant on player sales or property development to make money, so the core

business is improving. In previous years, much of the club’s excellent

financial performance has been down to profits from player sales (e.g. £65

million in 2011/12, £47 million in 2012/13) and property development (e.g. £13

million in 2010/11, £11 million in 2009/10).

Excluding those once-off factors would have meant that

Arsenal actually made substantial losses in the previous two years: £31 million

in 2011/12 and £45 million in 2012/13. This is now down to a far more

manageable £3 million loss in 2013/14.

Arsenal’s role as a pseudo property developer is largely

coming to an end with turnover down to £3 million, compared to £38 million the

previous season, which included the sale of the major site at Queensland Road.

The improvement in the football business last season is

clearly shown by the recovery in operating profit. This had been steadily

declining since 2009 with the club actually reporting operating losses of £18

million in 2011/12 and a worrying £33 million in 2012/13, but last season they

produced operating profit of £10 million.

However, this accounting profit includes non-cash items,

such as player amortisation, depreciation and impairment of player values. If

we add these back, we get yet another form of accounting profit, namely EBITDA

(Earnings Before Interest, Depreciation and Amortization). This metric has its

critics with the legendary investor Warren Buffett once cautioning, “References

to EBITDA make us shudder. It makes sense only if you think that capital

expenditure is funded by the tooth fairy.” That said, it is a useful proxy for

reviewing a club’s operating cash flow.

On that basis, Arsenal’s EBITDA more than doubled to a

highly impressive £62 million last season. On the one hand, this is still less

than half of Manchester United’s £130 million, but on the other hand it is

considerably higher than any other club in the Premier League (in 2012/13 the

next highest was Manchester City with £36 million).

Of course, Arsenal benefit from higher revenue than most

other clubs, though they fell to 8th place in the Deloitte Money

League for the 2012/13 season, as they were overtaken by the nouveaux riches of

Paris Saint-Germain and Manchester City, both boosted by large commercial deals

with the Qatar Tourism Authority and Etihad Airways respectively.

Gazidis has been quoted as saying, “Our revenues will grow

to put us into the top five revenue clubs in the world”, which is unlikely to

happen this season, as revenue also continues to grow at those clubs above

Arsenal in the Money League. In particular, Real Madrid, Barcelona and United

have all reported higher revenue for the 2013/14 season. For the 2014/15 season

Arsenal’s revenue will again rise due to the new PUMA kit deal, but the other

main driver, namely the new Champions League deal, will also help the other

clubs.

The most important revenue stream at Arsenal is Broadcasting

at £121 million, which has overtaken Match Day (£100 million) for the first

time since 2001. In fact, despite the advances made commercially, this revenue

stream still lags the others at £77 million. Over the last 5 years, Match Day

income is flat, while the growth drivers have primarily been Broadcasting,

which is up 65% (£48 million) due to central TV deals (Premier League and

Champions League), and Commercial income, which is up 60% (£29 million) mainly

due to the new Emirates shirt sponsorship.

Arsenal’s TV money increased by £36 million in 2013/14,

almost entirely due to the new Premier League deal, which saw Arsenal’s share

rise by £36 million from £57 million to £93 million. This increase is akin to

the old aphorism, “a rising tide lifts all boats”, as every Premier League club

benefits from this deal. That said, it still helps to be higher up the league

table, as the top club’s increase was £40 million (£57 million to £97 million),

while the bottom club “only” received an increase of £21 million (£41 million

to £62 million). Arsenal also received more facility fees for featuring in more

televised live games (25 compared to 22).

In contrast, Arsenal received less money from the Champions

League: €27 million (vs. €31 million) from the group stages onwards, as their

share of the TV market pool was lower (due to finishing lower in the Premier

League during the qualifying season and other English clubs progressing further

in the Champions League).

Nevertheless, the value of Champions League qualification is

clear, especially when looking at the Media revenue from the 2012/13 season,

where the four entrants earn significantly more than the other Premier League

clubs.

Indeed, the most earned by an English club in the Europa

League was Tottenham’s €6 million. The rewards (and differential) are even more

pronounced for the tournament winners: Champions League €57 million vs. Europa

League €15 million.

This effect will be even more pronounced from the 2015/16

season when the new Champions League deal commences. UEFA recently told the

European Club Association that clubs could expect a 30% increase in revenue,

but the uplift may be even higher for English clubs, as BT’s exclusive

acquisition of UK rights is double the current arrangement.

Although the growth in Match Day income was only £7 million,

the £100.2 million was the highest ever reported by Arsenal, slightly higher

than the £100.1 million in 2008/09. The increase was largely due to 3 more home

games (2 in the FA Cup and 1 in the Champions League), though the Emirates Cup

also returned after a break in 2012 for the London Olympics.

The Emirates stadium might not have the same atmosphere as

Highbury, particularly for those of my generation, but it has certainly been a

financial triumph. In fact, only Manchester United, Real Madrid and Barcelona

generate more money from Match Day income than Arsenal. All of this makes the

decision to raise ticket prices by 3% seem misguided at best, plain greedy at

worst.

Commercial revenue has long been Arsenal’s Achilles heel, as

the figures from the Deloitte Money League clearly demonstrate. Even the

2013/14 increase from £62 million to £77 million still leaves Arsenal back in

12th place and looks low compared to other leading clubs. OK, the

likes of Paris Saint-Germain £218 million and Manchester City £143 million may

benefit from “friendly” deals, but Arsenal are also way behind Bayern Munich

£203 million, Manchester United £189 million, Real Madrid £181 million and

Barcelona £152 million.

Arsenal’s £15 million increase this season is very largely

due to the extended partnership contract with Emirates, which benefited from 12

months in 2013/14, as opposed to only 6 months in the previous season. Against

that the club’s retail business was held back in the second half of the

financial year by lower available stocks of replica kit as part of the planned

transition from Nike to PUMA.

The club’s press release made great play of commercial

revenues rising by “more than 70%” since 2009, but that excluded the retail business.

Once this is combined to give total commercial income, the rise is more like

60%. That still sounds pretty good until you realise that this is essentially a

par performance with other clubs growing their commercial at a similar rate,

while the commercial colossus that is Manchester United has grown its revenue

by 171% in the same period with a veritable plethora of secondary sponsors

(surely Arsenal’s next area to be targeted).

Arsenal have already done pretty well with the new deals for

shirt sponsor and kit supplier. Although these are notoriously difficult to

compare, as they are rarely formally reported and contain many clauses based on

success on the pitch, sales targets, exchange rates, etc, it is clear that

Arsenal’s deals are among the best worldwide.

In fact, I reckon that only Manchester United’s Chevrolet

deal ($70 million or £43 million a year) is higher than Arsenal’s Emirates

deal. The £150 million contract covers a 5-year extension in shirt sponsorship

from 2014 to 2019 plus a 7-year extension in stadium naming rights from 2021 to

2028. This represents a significant improvement over the former deal: £90

million for 8 years shirt sponsorship plus 15 years stadium naming rights. The

club has not divulged how much of the deal is for naming rights, so I have

taken the straightforward £30 million annual figure, though my own estimate

would put the pure shirt sponsorship at around £26 million, which would still

be pretty good.

The PUMA kit deal only starts from 1 July 2014, so is not

included in the latest P&L figures. This is again worth £150 million over 5

years, so £30 million a year, which will represent a £22 million increase over

the former Nike deal. This is still dwarfed by Manchester United’s new £750

million 10-year deal with adidas that starts from the 2015/16 season, though

this would be reduced by 30% if United fail to participate in the Champions

League for two or more consecutive seasons (starting with the 2015/16 season).

There’s an old saying that “it’s an ill wind that blows no

good” which applies to Arsenal’s relatively poor commercial performance to

date. The new Premier League Financial Fair Play regulations restrict the

amount of money clubs can spend from the new TV deal on wages. Specifically,

clubs whose total wage bill is more than £52 million will only be allowed to

increase their wages by £4 million per season for the next three years. However

this restriction only applies to the income from TV money, so Arsenal’s

additional money from the new sponsorship deals can still be spent on wages.

Arsenal’s wage bill increased by 8% (£12 million) from £154

million to £166 million, largely due to the revised, improved contracts for

existing players, notably the “Brit Pack” (Wilshere, Walcott, Gibbs,

Oxlade-Chamberlain, Ramsey and Jenkinson) plus the package required to lure

Mesut Özil. Despite this increase, the wages to turnover ratio has actually

fallen from 64% to 56%, thanks to the higher revenue growth.

It is clear from the trend how much attention Arsenal pays

to the relationship between wages and revenue. In fact, in the last 5 years the

growth has almost been hand-in-hand, as wages growth of £62 million has been

covered by revenue growth of £74 million. If the club is to maintain a “safe”

ratio of 60%, that would imply a wage bill of £192 million on annual revenue of

£320 million (easily achievable once the PUMA increase is factored in), so the

club still has plenty of room to manoeuvre.

That would still be lower than the last reported wage bills

of Manchester City £233 million and Manchester United £215 million, but would

be more than Chelsea’s £173 million and Liverpool’s £133 million. What will be

particularly interesting is the impact that FFP has on clubs like Manchester

City, who admitted this was the reason they loaned Negredo to Valencia in the

summer, and Chelsea, whose wage

bill seems to have stalled and whose manager Jose Mourinho can (incredibly) now

be counted among its fiercest exponents – at least when discussing City.

Enough of the profit and loss account, the main financial

topic on the lips of Arsenal fans these days is that huge cash balance. Guess

what? It’s gone up again, rising another £55 million in the last 12 months from

£153 million to £208 million. For some reason the club’s headline statement

insists on reporting this as net of debt service reserves of £35 million,

giving the widely reported figure of £173 million, but the actual cash balance

is indeed north of £200 million.

To place that into context, the next highest cash balances

in the Premier League in the 2012/13 season were Manchester United £94 million,

Chelsea £26 million and Southampton £14 million. Since then, United’s 2013/14

balance has come down to £66 million, so Arsenal’s cash balance really is in a

class of its own, over three times as much as the next highest figure.

Of course, this figure is a bit misleading and not all of

this cash balance is available to spend on transfers. In fact, this is so

important that I’m going to say it again: not all of the £208 million cash is a

transfer fund.

This is due to many factors, including the fact that most

season ticket renewals are paid in April and May, so Arsenal’s cash balance

will always be at its highest when its annual accounts are prepared, namely 31

May.

In addition, there’s that annoying debt service reserve,

which has been around since the 2006 bond agreements, though it does raise the

question of whether these arrangements could be renegotiated given Arsenal’s

strong financial record, thus freeing up this £35 million.

The club also has to pay a good proportion of its annual

running expenses out of this cash, though other money will flow into the club

during the course of the season, such as TV distributions and merchandise sales

and the fact remains that year after year the cash balance has steadily risen:

May 2007 £74 million, May 2008 £93 million, May 2009 £100 million, May 2010

£128 million, May 2011 £160 million, May 2012 £154 million, May 2013 £153

million and May 2014 £208 million.

"Calum Chambers - Young Guns (Go For It)"

However, there are a couple of reasons why we still need to

be cautious with the cash figure. First, the club clearly stated that the cash

impact of the £64 million invested in new players during the accounts period

has been partially offset by the credit terms agreed with the vendor clubs. In

other words, Arsenal have not paid all the cash upfront, but (sensibly) agreed

stage payments, so part of the cash balance has to be reserved to pay sums due

on those transfers. This is reflected in the £53 million increase in creditors

falling due within one year from £150 million to £203 million.

Similarly, as these accounts were closed on 31 May, that

means that they do not take into consideration this summer’s transfer activity,

so another £50-60 million should be deducted from the reported cash balance.

On the other hand, Arsenal may well still be owed money from

sales of players to other football clubs, e.g. other debtors included £26

million in respect of player transfers as at May 2013.

"Welbz is Dat Guy"

In addition, the club has so-called contingent liabilities,

where payments are made to a player’s former club based on certain conditions

being met, e.g. number of first team appearances, trophies won, international

caps, etc. These amounted to £7 million in the 2012/13 accounts, but are by no

means certain to be paid – that’s why they are described as “contingent”.

There are other once-off factors that have helped inflate

Arsenal’s cash balance, such as property development, e.g. £20 million has come

from the Queensland Road site in the last two years, and upfront payments from

the new sponsorship deals with Gazidis stating that Emirates provided

additional money in advance last financial year in order that it could be

invested.

In short, without knowing all of the internal details, it’s

a mug’s game trying to predict how much Arsenal genuinely have available to

spend. It’s clearly not as much the £200 million in the books, but we can say

with some conviction that there would be enough available in the January

transfer window to cover the glaring weaknesses in the squad, let’s say £40-50

million.

Looking at Arsenal’s cash flow statement, we can see signs

of a change in approach: in the six seasons between 2007 and 2012 Arsenal spent

just a net £4 million on player purchases, while they have spent a net £37 million

in the last two seasons. Baby steps for sure, but steps in the right direction.

That said, most of the money still goes elsewhere. In

2013/14 Arsenal generated an impressive £96 million from operating activities,

spending £11 million on transfers, £19 million on financing the Emirates

Stadium (£12 million interest plus £7 million on debt repayments), £9 million

on capital expenditure (e.g. refurbishment of Hale End youth facilities) and £2

million on tax. What happened to the remaining £54 million? Nothing really, as

it just went towards increasing the cash balance.

This is nothing new. Since 2007 Arsenal have produced a very

healthy £526 million operating cash flow – that’s over half a billion. It’s

instructive how Arsenal have used this spare cash, spending £89 million on

capital expenditure, £135 million on loan interest, £77 million on net debt

repayments and £12 million on tax. Only 8% (£41 million) of the available cash

flow has been spent in the transfer market, though almost all of that has been

in the last two seasons. The other notable “use” of cash in that period is to

obviously increase the cash balance, which has risen by £172 million.

Clearly the debt incurred for the new stadium continues to

have an influence over Arsenal’s strategy. Although this has come down

significantly from the £411 million peak in 2008 to £240 million, it is still a

heavy burden, requiring an annual payment of around £19 million, covering

interest and repayment of the principal.

Although the net debt stands at only £33 million, thanks to

those large cash balances, the gross debt of £240 million remains the second

highest in the Premier League, only behind Manchester United, who still have

£342 million of debt even after all the Glazers’ various re-financings. Arsenal’s

debt comprises long-term bonds that represent the “mortgage” on the stadium

(£213 million) and the debentures held by supporters (£28 million).

Looking at the player trading over the last few years, we

can see that the club is beginning to walk the talk, as there has been a

noticeable change in the last three seasons with Arsenal no longer primarily a

selling club. In that period the club’s net spend was £95 million, which is in

marked contrast to the net sales of £49 million in the previous six seasons.

There’s no doubt that this parsimonious approach has put

Arsenal at a competitive disadvantage, exacerbated by the arrival of foreign

ownership with significant financial firepower. In fact, after the arrival of

Roman Abramovich at Chelsea, Arsenal have been heavily outgunned. Since the

2003/04 season, Chelsea and Manchester City have both splashed well over £500

million, while Arsenal were restricted to just £70 million. They were even

outspent by their North London neighbours, Tottenham (with £100 million), for

heaven’s sake.

But, as Bob Dylan said, the times they are a-changing. In

the last two seasons, Arsenal have spent a net £86 million, only just short of

Manchester City’s £114 million, but ahead of Chelsea and Liverpool. Manchester

United are the new big spenders, as Louis van Gaal attempts to build a new team

following the Moyes experiment (and Alex Ferguson’s retirement).

To sum up Arsenal’s financial condition, we could do a lot

worse than quoting Ivan Gazidis: “The club is in excellent shape, both on and

off the pitch”, adding that “we are well placed to deliver.” That is

undoubtedly true.

While not expecting a club like Arsenal to suddenly adopt a

“balls out, pedal to the metal” attitude, it is clear that something has

changed in Arsenal’s ability (and willingness) to spend.

In the past there has been more money available than the

club has utilised, but 2014 was always going to be the year of major change, as

the commercial deals were re-negotiated and the new TV deal came on line. The

big question is whether the additional money will make enough of a difference

on the pitch to take the club to the next level. Over to you, Arsène.